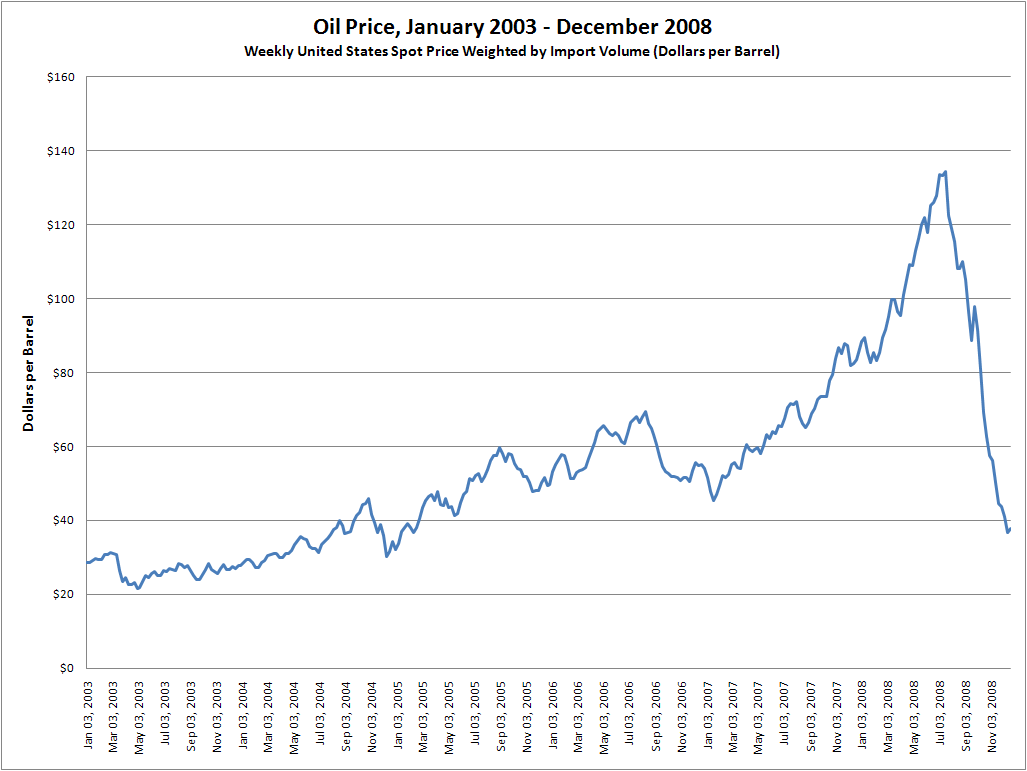

I was pretty smug in 2008.

Back in 2007, when oil hit $90 USD a barrel, I’d already traded in the gas guzzler for a small diesel and I made a plan to fill up six gigantic fuel tanks. When crude hit $147 in mid-2008, I was a freakin’ genius!

By 2009, oil was back at $40/barrel. You can’t win ’em all.

Fast forward to the pandemic. Convinced we’d see oil skyrocket as the recovery kicked in, I went out and bought two EVs and got solar panels installed… but then fuel stayed cheap!

Being right means nothing, if you’re early.

But here’s why I think this oil shock is different to the five we’ve had since 1973.

We’re vulnerable.

We don’t produce, or even refine oil, any longer…

And we depend on goodwill and handshakes from three main countries to keep us supplied…

We’re not worried about the cost of fuel – I am worried, though, about how most us will react when it’s clear government can’t save us.

I don’t believe in sugar coating it, but here’s the good news.

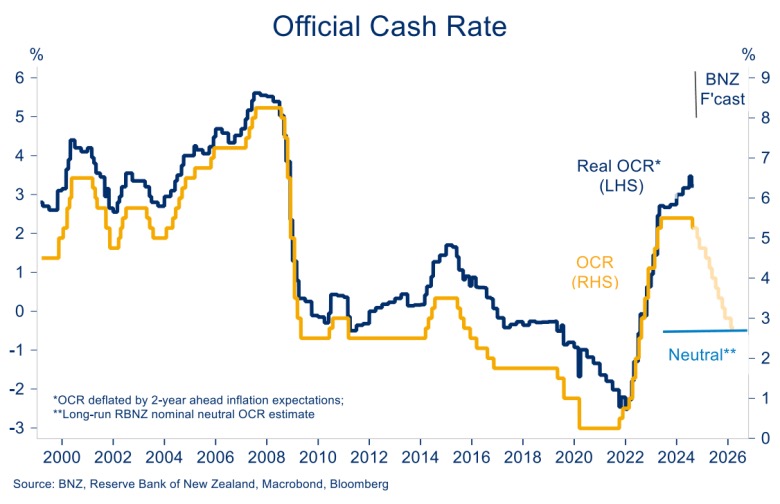

The mainstream take on interest rates is dead wrong.

The standard read goes like this: war, supply shock, higher oil, higher inflation, central banks hold rates or hike, your mortgage stays painful, for longer…yay.

It sounds logical. And it’s what we’re reading in the headlines right now.

But it mixes up two very different types of inflation. The inflation we’ve been fighting here in New Zealand, the kind that justified hiking the OCR to 5.5%, came from years of excess credit creation, quantitative easing, and policy error. That’s a monetary problem. Higher oil is a supply shock. It’s an external tax on growth, and it’s not the same thing as turning the money printer back on.

Different cause. Different treatment required.

Households don’t care if it’s higher interest rates, or higher fuel prices. They pull back on spending either way.

Throw into the mix the fact that New Zealand’s already at stall speed. Property’s been going backwards (adjusted for inflation) for years, and with anxiety around AI-induced mass unemployment, household confidence is struggling. If oil spikes hard and stays there, we don’t get a boom, we get a deep, dark recession.

The Reserve Bank can let higher oil costs do the same job as a higher OCR.

I know most think I’m wrong, but thankfully, I don’t care about being right. I care about blind spots. Here’s my thesis: oil and war become reasons for the RBNZ to reverse course.

Remember the Christchurch earthquakes? Remember the Covid (Delta) lockdown? All used as justification to lower rates which were already higher than they needed to be (in my view).

I believe the OCR will fall more than once over the coming period, and the seriousness of this oil shock only strengthens this conviction.

As an investor, what’s a rational response?

History across five oil shocks since 1973 is fairly consistent: panic selling is usually the wrong move. The worst market outcomes come from prolonged oil shocks. By the time you’re reading the breaking news, the repricing has already started.

The 1973 oil crisis, driven by the Arab oil embargo in response to the Yom Kippur War

The 1979 oil crisis caused by the Iranian Revolution

A brief spike in 1990 after Iraq invaded Kuwait

1999-2000 from OPEC production cuts

A surge in 2007-2008, driven by speculation ahead of the global financial crisis

In 2010-2011 due to the Arab Spring

2020-2022, post-Covid surge as the global economy reopened.

So here’s a couple things I’d be thinking about right now.

If you haven’t seriously thought about the future, and how you can align your own KiwiSaver and investment portfolio to it, then get in touch. Not to toot my own horn, but I’m really good at building investment strategies aligned with how people see the future.

If you have a solid income and time on your side, lower interest rates and a depressed property market is a gift!

Buying the bigger home, buying another investment property, buying a well-priced businesses with real pricing power, and building a portfolio around the future, rather than choosing one off the shelf...there is so much opportunity.

And if you want to hedge the bigger picture, in a global recession where governments spend more on defence, and the overall tax take falls… We know the central bank playbook now, and we know the value of ‘buying when there’s blood on the street’, so…

What becomes more valuable in a world of infinite credit creation? Scarce and finite forms of money.

The oil shock will pass. It always does. But the structural cracks it’s exposing in free trade ideologies, supply chain dependency, and government deficits don’t get fixed by themselves.

In summary, I can’t say times won’t get tough for a few years, but but based on the past, time and time again, the answer appears to be the same: Just stay invested.

Changing things up based based on current events may not be the best move right now, because prices have already factored in all known information. However, when the dust has settled, and if you want to review your long-term strategy, talking it through can help you feel better.